The African insurance industry is predominantly group life insurance business, and due to limited spending power there has been much slower uptake of individual insurance policies.

Poverty has been reduced somewhat in Africa but this is primarily in the lowest income bracket of the middle class who are prone to falling back into poverty.

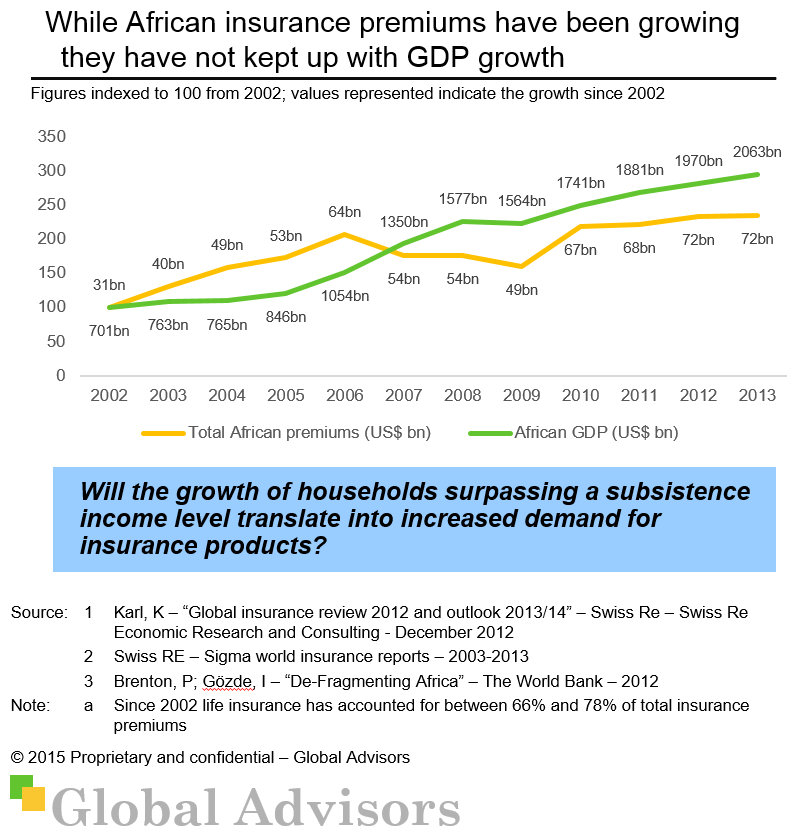

Furthermore, policyholders are typically unaware or sceptical of the benefits of owning insurance products, they are difficult to reach and often do not earn regular incomes.1

Microinsurance products are growing more quickly – this presents an opportunity for targetting lower income groups.