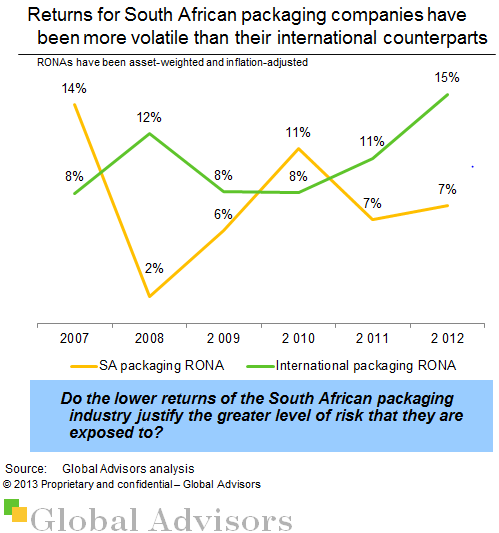

The average, real Return on Net Assets (RONA) between 2007 and 2012 was 7,8% for South African packaging companies, and 10,4% for international packaging companies

RONAs have been calculated for listed-packaging companies and are asset-weighted and adjusted for average annual inflation. International companies are primarily from the USA and UK, as well as Finland and Australia. South Africa faces a greater level of risk due to the country risk and volatility of returns.